If there is anything that ought to be taught in school that is not, it’s “financial literacy.” Many of us wouldn’t consider ourselves financially educated. We can balance our bank accounts (maybe) and keep our credit cards paid (usually) — but financial literacy is something we leave typically to accountants and bankers. But financial literacy in divorce is crucial.

True financial literacy, like computer literacy, means having the skills needed to handle money at all levels — not just budgeting for a week, but for a year or five. You should understand different kinds of retirement funds, alternate income sources, and ways to clear debts.

You need these skills before an emergency strikes, such as a divorce. You may have an attorney or mediator to help you, but you need to understand what your attorney is talking about before you put your signature on any agreement.

Understanding Your Financial Future

Divorce can be an unnerving and financially destabilizing event in someone’s life. Even when the separation is amicable, property must be divided, bank accounts and pension plans split up, and words like “qualified domestic relations order” start being thrown around. It helps if you know what they’re talking about in terms of your future.

If you’re going through (or about to go through) a divorce, now is the time to brush up your financial literacy and find out what is happening.

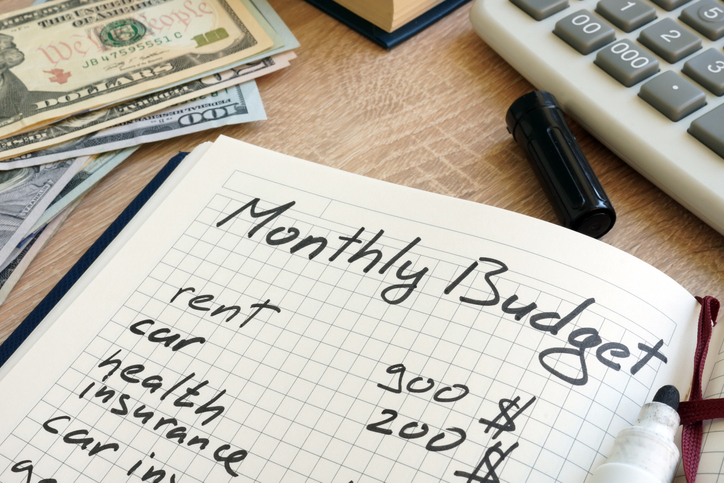

Estimating Expenses and Costs

In divorce proceedings, the approach to estimating expenses and costs varies between traditional litigation and mediation.

Divorce Litigation:

In traditional divorce litigation, the focus is often on short-term financial information to determine how assets will be divided. When you review your divorce paperwork, there is typically a section for estimated monthly expenses. The courts use this information as a basis for asset division. It is essential to accurately assess your expenses. Instead of simply estimating, “I spend $100 per week on groceries,” take the time to track your actual weekly expenditures on food, including quick trips to convenience stores and stops at Starbucks for coffee. This detailed tracking helps you understand your spending habits better and enhances your budgeting skills. Importantly, during financial negotiations in divorce litigation, you can present your actual expenses to justify your financial needs.

Divorce Mediation:

In contrast, divorce mediation encourages a collaborative approach to financial planning. Rather than focusing solely on estimated monthly expenses, mediation emphasizes open communication and shared decision-making. Both parties work together to create a comprehensive budget that reflects their individual and joint financial needs. This collaborative process often leads to a more nuanced and fair division of assets, as it takes into account the specific financial circumstances and priorities of both parties. Financial literacy plays a crucial role in mediation, empowering both parties to make informed decisions and achieve a mutually beneficial resolution.

Understand the Implications of Budgets

Once you know what your expenses are each month, you’re in a better position to negotiate during your divorce.

Some divorce advisors recommend creating three different budgets:

- A historical or “lifestyle” budget. This is how you’ve spent money during your marriage.

- A temporary budget for your divorce. This will include any divorce-related expenses, such as travel time and court costs.

- A post-divorce budget that will contain any alimony or support payments

Gather your financial documents and review them carefully when making your budgets. Your historical budget will help you make plans for your future financial plans.

Long-Term Financial Goals

After a divorce, many people feel adrift. Even if you have a good job and your divorce settled your financial affairs equitably, you may feel at a loss about your future goals. Now is a good time to review those budgets you made and make better long-term plans for yourself and your family.

Use your historical budget to plan for the future. Your divorce can be a chance to start fresh. Now is a good time to discuss financial planning. Start with your daily and weekly needs. There are things you cannot do without, and things you must pay, such as the power bills. At the same time, don’t force yourself to live in a hovel—budget enough for comfort.

- Review your fixed and variable expenses. Where can you cut costs and what must you have every month? Perhaps now is a good time to buy a home coffeemaker and skip the daily double latte.

- Will you be paying or receiving monthly support payments? If you must make child support payments, consider having them deducted from your paycheck rather than making direct payments to your former spouse. This ensures timely payments, and lets you make your monthly budgeting plans with that amount already deducted from your available funds.

- If you and your spouse are dividing a retirement or pension, consider paying or receiving the amount in a lump sum during the divorce, rather than cashing out the pension. This preserves the pension for its intended purpose, providing income after retirement.

Planning Your Financial Future

In times past, divorce meant that one party had a drastic decline in their financial status, while one party’s improved. Fortunately, things have changed, but without some forethought, you can still find yourself struggling after the divorce.

Resist the temptation to return to your former pre-divorce spending habits. Remember, even if you receive child support or other payments, it won’t be the same as when you and your partner were paying for everything between you.

If you receive any lump sum payments from the settlement agreement—for instance, if you divide property and take your share of a house or car in cash—consider investing or purchasing a 401(k) rather than spending it. Or pay down existing debts to improve your credit score.

Consider discussing your situation with a divorce financial analyst. Your attorney or mediator may be able to suggest someone who can help you. They can explain financial planning and review investment methods that fit your income and lifestyle.

Final Thoughts

At Divorce With Dignity, Providers can empathize with what you’re going through emotionally and financially. We try not to use confusing terminology like “forensic accounting” and when we do, we’ll always explain what it means and why you need it. We want to see you and your former partner divide your assets in ways that help both of you separate and move on successfully with your lives.

If you need additional help, we want to help you find that too. Don’t feel like you’re adrift in a strange sea of dollars and nonsense. If you have questions with no answers, just ask our providers. If we can help you find the answers, our Providers are just a phone call away.